The Economic Collapse

February 11, 2012

February 11, 2012

Do you want to see what a 21st century economic depression looks like? Just look at Greece. Once upon a time, the Greek economy was thriving, the Greek government was borrowing money like there was no tomorrow and Greek citizens were thoroughly enjoying the bubble of false prosperity that all that debt created.

Those that warned that Greece was headed for a financial collapse were laughed at and were called “doom and gloomers”. Well, nobody is laughing now. You see, the truth is that debt is a very cruel master. Greeks were able to live way beyond their means for many, many years but eventually a day of reckoning arrived.

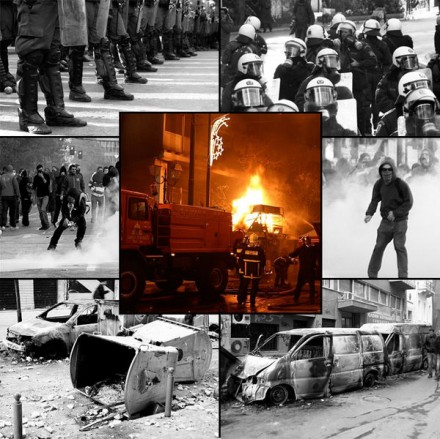

At this point, the Greek economy has been in a recession for five years in a row, and the economic crisis in that country is rapidly getting even worse. It was just recently announced that the overall rate of unemployment in Greece has soared above 20 percent and the youth unemployment rate has risen to an astounding 48 percent. One out of every five retail stores has been shut down and parents are literally abandoning children in the streets. The frightening thing is that this is just the beginning. Things are going to get a lot worse in Greece. And in case you haven’t been paying attention, these kinds of conditions are coming to the United States as well. We are heading down the exact same road as Greece went down, and the economic pain that this country is eventually going to suffer is going to be beyond anything that most Americans would dare to imagine.

All debt spirals eventually come to an end. For years, Greece borrowed huge amounts of very cheap money, but there came a point when the debt became absolutely strangling and the rest of the world refused to lend the Greek government money at such cheap rates anymore.

Greece would have defaulted long before now if the EU and the IMF had not stepped in to bail them out. But along with those bailouts came strings. The EU and the IMF insisted that the Greek government cut spending and raise taxes.

Well, those spending cuts and tax increases caused the economy to slow down. Tax revenues decreased and deficit reduction targets were missed. So the EU and the IMF insisted on even more spending cuts and tax increases.

Even after all of the spending cuts and all of the tax increases that we have seen, the debt to GDP ratio in Greece is still higher than it was before the crisis began. Today, the Greek national debt is sitting at 142 percent of GDP.

Now the EU and the IMF are demanding even more austerity measures before they will release any more bailout money.

Needless to say, the Greek people are pretty much exasperated by all of this. They created this mess by going into so much debt, but they certainly don’t like the solutions that are being imposed upon them.

Protesters in Greece are absolutely outraged that the EU and the IMF are now demanding a 22 percent reduction in the minimum wage.

Most families in Greece are just barely surviving at this point. Unfortunately, Greece is probably looking at depression conditions for many years to come.

Over the past three years, the size of the Greek economy has shrunk by 16 percent.

In 2012, it is being projected that the Greek economy will shrink by another 5 percent.

Sadly, that projection is probably way too optimistic.

No comments:

Post a Comment