April 16, 2015

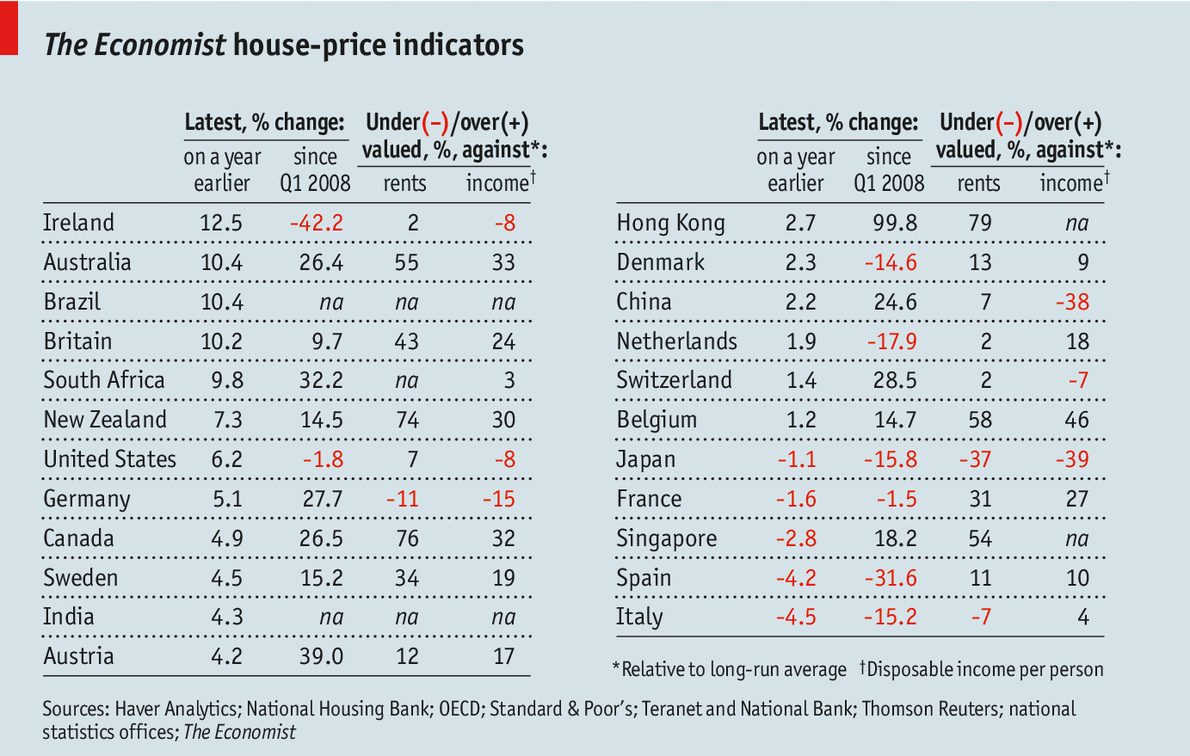

BEFORE the financial crisis of 2007-08 low long-term interest rates fuelled an extraordinary house-price boom around the world. That bubble was pricked in the crisis and subsequent recession. Since then, however, central banks’ attempts to crank up the recovery by pushing down long-term interest rates to new lows have had a predictable consequence in many property markets. House prices are now rising in 18 of the 23 economies that we track, in eight of them at a faster pace than three months ago (see table).

There remain some weak spots, especially in Europe. Prices in Spain, which had one of the biggest bubbles before the crisis, are still falling. They have also been declining in France and Italy, reflecting continuing economic weakness in the euro zone’s second- and third-largest economies. In contrast, housing markets are buoyant in some northern European countries, notably Britain.

Since some recovery was bound to occur after the housing slump, how worrying are the renewed signs of exuberance? To assess whether house prices are at sustainable levels, we use two yardsticks. One is affordability, measured by the ratio of prices to income per person after tax. The other is the case for investing in housing, based on the ratio of house prices to rents, much as stockmarket investors look at the ratio of equity prices to earnings. If these gauges are higher than their historical averages then property is deemed overvalued; if they are lower, it is undervalued.

Based on an average of these measures, houses are at least 25% overvalued in nine countries. Judged by rents, the most glaring examples are in Hong Kong, Canada and New Zealand. The overshoot in these economies and others bears an unhappy resemblance to that prevailing in America at the height of its boom before the crisis.

No comments:

Post a Comment